Financial Literacy Month

April is Financial Literacy Month. Check out our podcasts, videos, articles, songs, lesson plans and activity guides, we’ve got something for everybody.

April is Financial Literacy Month. Check out our podcasts, videos, articles, songs, lesson plans and activity guides, we’ve got something for everybody.

Multi-family homes are a hot commodity in real estate. But what exactly are they, who buys them and what are the different paths to purchasing?

Thinking about buying a home? This detailed Homebuyer's Playbook is the resource you have been looking for.

Rockland Trust offers both consumer and business credit cards designed to meet your unique needs.

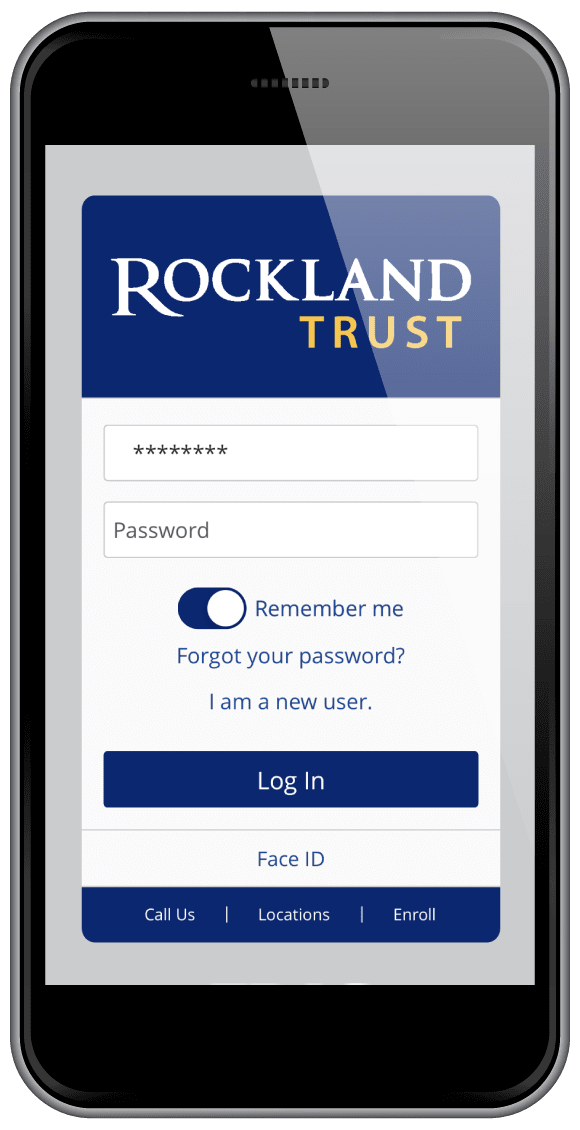

We know your time is valuable. That's why we make it as easy as possible to take care of your financial business online and with your mobile device.